Is Embedded Insurance Changing the Insurance Landscape?

The insurance industry, traditionally associated with complicated terms and hidden exclusions, might be on the brink of transformation to regain the trust of policyholders.

This evolution is embodied by embedded insurance. Incorporating coverage directly into the purchase of goods or services, embedded insurance provides immediate protection for the items and services that people commonly use.

This isn’t just a marketing ploy but an emerging strategy aiming to regain trust from a sceptical generation and bridge the notable “protection gap,” which leaves many without adequate coverage.

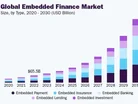

Research by Boston Consulting Group (BCG) indicates that embedded insurance is expected to grow from US$13bn to more than US$70bn in gross written premiums by the decade's end, hinting at a potential transformation within the insurance sector.

Embedded Insurance: Explained

Embedded insurance shifts away from standalone products, leaning towards seamless integration, such as travel protection automatically offered at flight checkout, device insurance bundled with a new phone like AppleCare, or instant liability cover included with every Airbnb stay.

Previously seen as checkout add-ons, advancements in APIs and data analytics now render these offerings invisible, automatic and expected during digital-first purchases.

Reasons Behind Its Growing Popularity

The World Economic Forum (WEF) notes that there’s an expanding “protection gap” — a disparity between the coverage people possess and what they actually require.

This gap is particularly evident among younger generations.

Data from Fintech Ventures highlights that the protection gap doubled from 2000 to 2020 due to urbanisation, climate-related events, and a persistent lack of real innovation.

"Millions have now been left underprotected or overpaying for policies they don’t even understand," says Aaron Sherwood, Founding Curator of Global Shapers, London Hub II and Agenda Contributor at the WEF.

A LIMRA study finds only 48% of Millennials and 40% of Gen Z have life insurance, with nearly half feeling underinsured, citing cost and lack of clarity as primary obstacles.

Traditional insurance models risk alienating the very consumers they need for survival.

Bridging the Protection Gap

Regaining trust requires more than simplifying the purchasing process for insurance.

The WEF emphasises that real-time, data-driven personalisation is crucial to the success of embedded insurance and presents a groundbreaking promise, especially for a younger, tech-savvy populace.

The transparent use of AI in this context can tackle long-standing issues related to claims, pricing, and coverage comprehension.

Accenture reports that six in 10 consumers are willing to share substantial personal data if it results in fairer pricing and coverage that better suits their needs.

"The real advantage, though, is that embedded insurance thrives through collaboration, not just isolation," Aaron adds.

"Traditional insurers bring underwriting expertise, while insurance technology provides technological advancement. Consumer brands offer everyday trust and data interaction points that traditional players could never reach."

By 2028, more than 30% of insurance transactions are predicted to occur through embedded channels, according to EY.

However, growth isn’t sufficient: unless experiences offer genuine value and transparency, technology risks enlarging, instead of solving, the trust deficit.

Aaron adds: "This is where real-time, data-driven personalisation becomes a game-changer, particularly for a younger, tech-savvy generation that expects everything to be tailored and instant. Better data can create personalised protection, highlighting the imperative to reinvent or become irrelevant.

"A new wave of technology is already in people’s hands. The future of insurance will be shaped by the brands willing to show up transparently, partner with innovators, use data responsibly and prioritise people, not just profits, first."